How Embedded Finance is Redefining FinTech in India

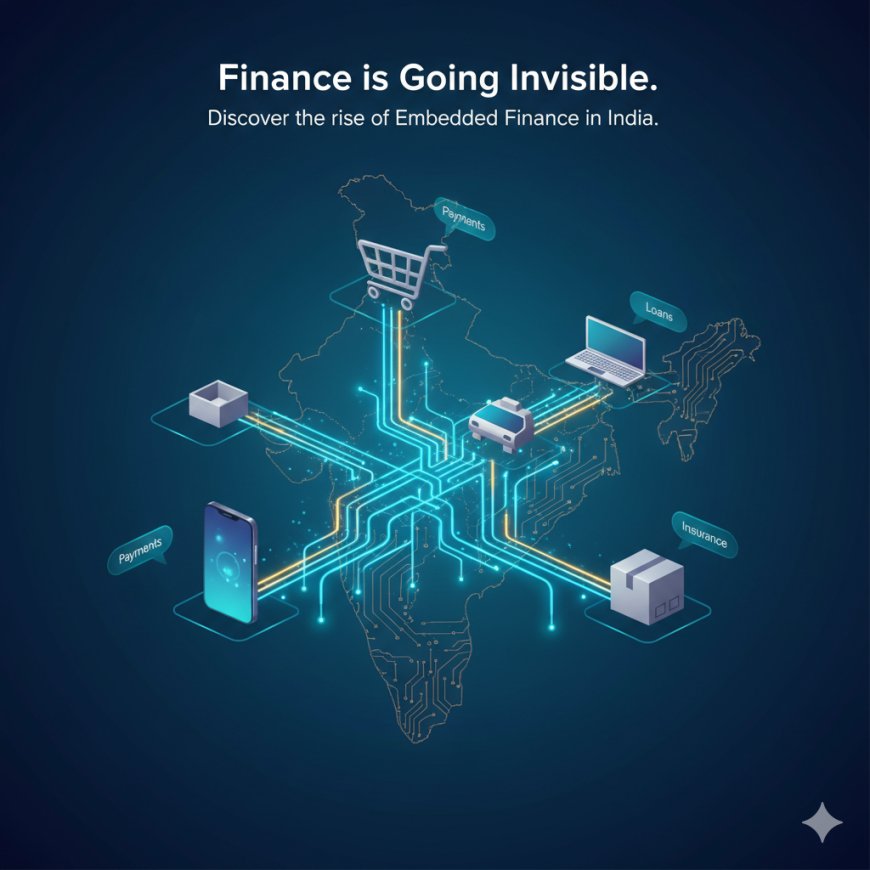

Embedded Finance & FinTech Beyond Payments: Explore how financial services are becoming invisible yet indispensable — seamlessly integrated into everyday apps and industries across India. Learn what’s driving this silent fintech revolution and why embedded finance is redefining the future of business.

When you book a cab, order groceries online, or buy your next phone on an e-commerce site, chances are you’re using financial services without even realizing it. You might split the payment into easy EMIs, use a “buy-now-pay-later” option, or get a quick refund credited instantly to your wallet. All of this happens quietly in the background — no bank visits, no paperwork, no waiting.

Welcome to the age of embedded finance — where financial services are no longer a separate experience but an invisible layer woven into our everyday lives.

Traditionally, finance meant dealing directly with banks, insurers, or investment platforms. But that line is blurring fast. Today, non-financial companies — from cab aggregators and online retailers to logistics firms and SaaS startups — are becoming providers of financial solutions. They’re doing this not by turning into banks, but by embedding financial capabilities directly into their apps and platforms.

Think about it this way:

Your favorite food delivery app can now offer credit to restaurants, insure its delivery partners, and process instant digital payments — all without being a bank. That’s the magic of embedded finance.

It’s fintech, but with a twist — finance without the “fin.” It’s seamless, convenient, and increasingly essential to how modern consumers and businesses operate.

This shift represents the next wave of financial innovation — one where finance moves from being a standalone service to a silent enabler across industries. And for India, a country with deep digital penetration and millions of small businesses, the potential is massive.

In short: the future of fintech isn’t about more apps — it’s about smarter integration.

Understanding Embedded Finance

So, what exactly is embedded finance?

In simple terms, embedded finance allows companies to offer financial services within their own platforms — without becoming full-fledged financial institutions.

They do this through partnerships with banks and fintech companies, often powered by APIs (Application Programming Interfaces) that connect these systems seamlessly.

Here’s how it works in everyday life:

- Buy-now-pay-later (BNPL): When you shop online and choose to pay in installments, you’re using embedded lending. The e-commerce platform integrates with a lending partner to offer you instant credit — no separate bank login needed.

- Ride-hailing apps: Drivers on platforms like Ola or Uber can now access instant loans, insurance, or fuel credit directly from the app — helping them manage daily expenses without traditional banking hurdles.

- SaaS platforms for small businesses: Software providers like RazorpayX or Zoho Books integrate payment gateways and banking tools so that business owners can manage invoices, receive payments, and even access credit — all in one place.

Behind these experiences are powerful APIs and open banking frameworks that securely link banks, fintechs, and digital platforms. These connections make it possible for financial services to move beyond traditional boundaries — from banks to wherever the customer already is.

It’s also a data-driven revolution. Every transaction, user behavior, and payment history helps companies offer more personalized and faster financial solutions — from credit scoring to customized insurance plans.

And the scale of this opportunity is enormous.

According to Statista and PwC, India’s embedded finance market is projected to reach $21 billion by 2029, growing at over 25% annually. The drivers?

- The rise of digital-first consumers

- Government-backed infrastructure like UPI and Aadhaar

- And the increasing appetite of businesses to integrate financial tools directly into their offerings.

In essence, embedded finance is making financial access simpler, faster, and more inclusive. It’s not just changing how we pay — it’s redefining how we experience money altogether.

Beyond Payments: The Expanding FinTech Horizon

For a long time, “fintech” mostly meant payments — apps that helped you transfer money, pay bills, or shop online. But that was just the beginning.

Today, embedded finance is expanding far beyond payments — reaching into lending, insurance, wealth management, and even payroll. It’s not just about moving money anymore — it’s about making money work smarter across platforms we already use every day.

Here’s how it’s evolving:

Embedded Lending

When a small business sells on a marketplace like Amazon or Flipkart, the platform already knows its revenue and growth patterns. Using this data, it can offer pre-approved loans instantly — no collateral, no lengthy forms. This kind of credit access is helping thousands of SMEs grow faster.

Embedded Insurance

From booking travel insurance with your flight ticket to insuring a smartphone right at checkout — embedded insurance is now everywhere. The process is quick, transparent, and usually more affordable because it’s offered at the point of need.

Embedded Investments

Some platforms are even helping users invest while they shop or save automatically. For example, fintechs integrate mutual fund or micro-investment options within everyday apps, letting users grow their wealth passively.

Embedded Payroll & HR Tools

In the business world, HR tech and SaaS platforms are embedding financial tools like salary advances, employee wallets, and tax-saving calculators. This gives employees more flexibility and control — without depending on traditional banks for every need.

All these examples point to one big shift: finance is becoming a built-in feature, not a separate service.

And for users, it feels effortless. You don’t need to “go to a bank” — because the bank comes to you, right where you already are.

As India continues to digitalize everything from healthcare to education, we’ll see even more industries embedding financial tools — making money management an invisible, yet powerful part of everyday life.

Why It Matters: The Business Advantage

For businesses, embedded finance isn’t just a nice add-on — it’s becoming a serious competitive advantage.

Think about it: every time a brand helps customers pay easily, access credit faster, or insure what they buy — it’s not just offering convenience; it’s building trust and loyalty.

Here’s how embedded finance is changing the game for businesses of all sizes:

Better Customer Experience

Customers love convenience. Whether it’s one-click payments or instant EMI approvals, frictionless finance keeps people coming back. Businesses that make financial interactions simple often see higher sales and stronger retention.

New Revenue Streams

Companies are discovering new ways to earn. By partnering with fintech providers, they can share in transaction fees, earn from interest spreads, or offer premium financial features to customers.

For example, a travel portal that offers travel insurance earns a small cut from every policy sold — without doing the underwriting itself.

Deeper Data Insights

When businesses handle financial interactions directly, they get richer customer data — spending habits, preferences, timing, etc. This helps them create personalized offers and improve decision-making.

Inclusion & Reach

Embedded finance also opens doors for small businesses and rural consumers. Through partnerships and digital tools, financial access is expanding to places where traditional banks never reached. For example, micro-insurance and instant digital credit have empowered local shopkeepers and gig workers across India.

Example in Action

Take the example of PhonePe and Flipkart. What started as a simple payments integration has evolved into an entire financial ecosystem — including insurance, mutual funds, and credit. This integration keeps users within the same ecosystem longer, improving engagement and revenue for both companies.

In short, embedded finance helps businesses grow faster, smarter, and closer to their customers.

It blurs the line between financial and non-financial — and in doing so, creates value for both sides.

The Challenges of Going Deep

Of course, every big shift comes with its share of challenges — and embedded finance is no exception.

While the concept sounds simple, the execution is anything but. To make financial tools truly seamless, companies need to balance innovation with security, regulation, and user trust. Let’s look at the key hurdles:

Regulatory Complexity

Finance is one of the most tightly regulated industries in the world — and for good reason. When non-financial companies start offering loans, payments, or insurance, they enter a space governed by the RBI, SEBI, IRDAI, and multiple compliance frameworks.

For example, India’s Digital Lending Guidelines tightened norms around BNPL and fintech credit services to protect consumers. This means every embedded finance partnership must ensure transparency, proper licensing, and data protection.

Data Security & Privacy

Embedded finance runs on data — from spending patterns to identity verification. That’s why cybersecurity and consent management are non-negotiable. Any breach or misuse of personal financial data can quickly erode user trust.

As India adopts stricter data laws like the Digital Personal Data Protection Act (DPDP), 2023, platforms need to ensure full compliance to avoid risks.

Integration & Technical Hurdles

While APIs make embedded finance possible, integrating multiple systems — banks, fintechs, and business platforms — can be tricky. Compatibility issues, system downtimes, and inconsistent user experiences can slow adoption.

User Awareness & Trust

Many first-time users still hesitate to use financial features on non-financial apps. For instance, a customer might be unsure whether a loan offered via an e-commerce site is legitimate.

Building clarity and confidence through education and transparent communication is essential to win over this new wave of digital consumers.

Partnerships & Profitability

Finally, for embedded finance to truly scale, banks, fintechs, and platforms need to work in sync. But aligning on profit-sharing, risk management, and customer ownership can be a balancing act.

Despite these challenges, the direction is clear — the ecosystem is evolving, and every stakeholder is learning fast.

As one fintech founder put it recently:

“Embedded finance is not about replacing banks — it’s about reimagining how people experience financial services.”

The Road Ahead: FinTech Beyond Boundaries

The future of embedded finance in India looks nothing short of transformative.

We’re already moving from payments and credit to more personalized and predictive financial ecosystems.

Here’s where things are headed:

Expansion Across Sectors

Expect to see embedded finance enter newer areas — healthcare, education, logistics, and even agriculture. Imagine farmers accessing instant crop insurance via an agri-tech app, or students getting low-interest education loans directly through online learning platforms.

Smarter, AI-Powered Finance

Artificial Intelligence (AI) will play a key role in personalizing financial offerings. From automated credit scoring to customized insurance premiums, data-driven intelligence will help platforms offer faster and fairer financial access.

Rise of Embedded Wealth & Investments

Just as UPI revolutionized payments, the next wave could democratize investing. We may soon see embedded mutual fund, SIP, or even digital gold options inside lifestyle apps — making investing as easy as online shopping.

India’s Global Leadership

India already leads the world in digital transactions — with over 130 billion UPI transactions in FY 2024, surpassing even China. With the government’s push toward Open Credit Enablement Networks (OCEN) and Account Aggregators, India could become a global benchmark for embedded finance innovation.

Inclusion at Scale

Perhaps the most powerful outcome will be financial inclusion. Embedded finance bridges the gap for small-town consumers, gig workers, and informal entrepreneurs who often fall outside the traditional banking net.

In essence, this isn’t just about financial convenience — it’s about economic empowerment.

Wrap-Up: The Invisible Revolution

Embedded finance is quietly reshaping the way India transacts, saves, borrows, and invests.

It’s turning everyday apps into financial hubs — and everyday consumers into empowered participants in the digital economy.

For businesses, it’s an opportunity to create deeper relationships and new revenue streams.

For users, it’s convenience, inclusion, and choice — all rolled into one seamless experience.

The most powerful revolutions are often the ones you don’t notice happening — and embedded finance is exactly that.

It’s invisible, yet everywhere.

And as it continues to evolve, it will redefine not just fintech — but the very future of how India experiences money.

What's Your Reaction?

Like

1

Like

1

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0