The Future of Indian Fintech Built on Compliance and FraudTech Strength

India’s fintech industry is undergoing a major reset as RBI tightens digital lending, KYC, FLDG, and UPI fraud rules. This article explains how compliance, AI-driven risk scoring, and advanced FraudTech are becoming the core survival factors for fintechs in 2025 — redefining which players scale and which exit.

India’s fintech ecosystem has entered its most defining transition since UPI was launched. What began as a decade of hyper-growth, massive user acquisition, and rapid product experimentation has now shifted into a compliance-first, audit-ready, stability-driven era. This shift is not cosmetic — it is structural, inevitable, and long overdue.

How India entered a new compliance-first era

Over the past few years, three things happened simultaneously:

- Digital lending exploded — from BNPL to instant personal loans, millions of customers were onboarded at unprecedented speed.

- UPI hit mass adoption — touching 1,000+ crore transactions a month.

- Fraud became industrialised — from mule accounts to deepfake KYC, phishing, and UPI switch fraud.

This combination created a perfect storm. And the RBI responded.

Why RBI’s tightening is not a setback — but a survival filter

Many founders saw the wave of circulars and restrictions as a brake on innovation. In reality, the RBI is filtering out weak, non-compliant, and high-risk players who scaled without guardrails.

The new regulatory environment favours fintechs that:

- Have solid balance sheets

- Treat consumer protection as a core product feature

- Invest in real-time fraud controls

- Operate within clear partnership boundaries

In short: 2025 is the year when “growth at any cost” died, and “compliant by design” became the baseline.

Digital lending + UPI scale = unprecedented fraud risks

The bigger the system, the bigger the attack surface. India is now the world’s largest real-time payments ecosystem — and that has made fraudsters more sophisticated and organised.

Some emerging risks include:

- AI-generated fake KYC videos

- Deepfake voice-based loan applications

- Social engineering that targets UPI intent flows

- Loan stacking across multiple apps

- First-party fraud disguised as customer disputes

Fintechs can no longer rely on rule-based systems or manual reviews. Fraud has become a real-time, AI-powered battle — and only AI can counter AI.

Thesis: Only fintechs that master compliance + AI-driven FraudTech will thrive

The fintech winners of 2025 won’t be the ones with the flashiest app or the quickest onboarding. The winners will be those that:

- Build RBI-aligned, audit-ready systems

- Deploy AI-driven risk scoring, behavioural biometrics, and real-time fraud detection

- Adopt ethical, transparent lending practices

- Strengthen data governance and repayment discipline

This is the Great Fintech Reset — not a slowdown, but a transformation where compliance becomes strategy, and FraudTech becomes the new moat.

RBI’s New Rulebook: What Changed & Why

The Reserve Bank of India has rolled out the most sweeping reforms in India’s fintech history. These changes redefine how digital lenders, NBFCs, and fintech partners operate.

Overview of the major regulatory shifts

1. Digital Lending Guidelines 2.0

RBI’s updated digital lending norms emphasise:

- Direct disbursal and repayment between borrower and the regulated entity (no pass-through wallets)

- Full transparency on APR, fees, and recovery processes

- Consent-based data access with strict privacy checks

- Cooling-off period for loan cancellations

- Ban on misleading or high-pressure loan apps

This eliminates predatory players and forces clarity, accountability, and consumer trust.

2. FLDG Caps & Balance Sheet Responsibility

Tight restrictions placed on First Loan Default Guarantee (FLDG) arrangements:

- Caps on loss-sharing

- Clear disclosure of credit risk ownership

- Banks/NBFCs must maintain full balance sheet responsibility

This ends the era of “asset-light” shadow lending and brings real discipline to underwriting models.

3. Tightened KYC & Repetitive Fraud Checks

The focus is now on continuous KYC, not just onboarding. Rules emphasise:

- Re-authentication for high-risk users

- Biometric + video KYC cross-validation

- Device fingerprinting

- Flags for duplicate PAN, Aadhaar misuse, or mule accounts

- Mandatory fraud registries and bureau checks

Essentially, KYC is no longer a one-time event — it is now a lifecycle obligation.

4. New UPI Fraud Liability & Dispute Resolution Rules

With UPI fraud cases rising, RBI intervened decisively:

- Faster turnaround for reversing fraudulent debits

- Liability assigned based on “authenticity of consent”

- Fintech PSPs must deploy real-time anomaly detection

- Stricter monitoring of merchant onboarding and mules

- Mandatory reporting of fraud within defined timelines

These rules protect consumers while forcing ecosystem players to invest in superior security.

The Intent Behind the Rules: Fix the Foundations

The RBI’s objective is clear:

- Stop predatory lending practices

- Prevent data harvesting and misuse

- Protect low-income borrowers from aggressive recovery

- Avoid systemic risk as fintechs grow

- Ensure UPI remains secure and internationally reputable

This is not regulation for the sake of regulation — it is building the foundation for responsible fintech at global scale.

Impact on Fintechs, NBFCs & Banks

Fintech Startups

- Must undergo compliance overhauls

- Will need stronger bank/NBFC partnerships

- Must invest in FraudTech, AI scoring, and governance tools

- Product launches will slow, but quality will rise

NBFCs

- Gain a stronger position as balance-sheet owners

- Must upgrade underwriting and risk frameworks

- Face more scrutiny on FLDG and capital adequacy

Banks

- Benefit from increased trust and regulatory alignment

- Gain more power in digital lending partnerships

- Must improve real-time fraud analytics to protect UPI rails

Overall:

Only the most compliant, fraud-resilient, and AI-enabled players will survive the 2025 fintech reset.

The Digital Lending Boom: Growth Meets Complexity

Over the past three years, India has witnessed one of the world’s fastest surges in digital credit. Consumer loans, small-ticket BNPL, micro-lending apps, and algorithm-driven MSME credit have reshaped how Indians borrow. What used to take days—paperwork, branch visits, manual underwriting—now takes seconds on a smartphone.

A Credit-Hungry Market That Attracts Every Fintech

India’s demographic and economic structure makes it a dream market for digital lenders:

· A rapidly growing middle class

· Rising aspirations for consumption

· Low credit card penetration

· Millions of thin-file or invisible consumers

· MSMEs desperate for short-cycle working capital

(where traditional banks remain too slow)

This has opened the door for new-age fintechs, lending service providers (LSPs), and NBFC–fintech partnerships to capture demand at scale. The result?

Digital loan disbursals crossed historic highs between 2022–2025.

But this speed comes at a cost.

High-Speed Onboarding ≠ High-Quality Underwriting

Most fintechs optimized for rapid growth, not risk discipline:

· Automated onboarding often ignores deeper identity signals.

· AI scoring models use limited behavioural data.

· Collateral-free loans increase exposure.

· FLDG structures incentivized aggressive customer acquisition.

This created a perfect environment for fraud and delinquency to explode.

The Hidden Risks Beneath the Growth Curve

With growth came complexity:

· Rising defaults, especially in small-ticket personal loans and BNPL

· Account takeovers (ATO) from SIM swap, phishing, and OTP-harvesting

· Mule accounts becoming intermediaries for UPI fraud

· Circular lending—multiple loans across apps before repayment

· Repeat borrowers re-entering the system through loopholes

The message is clear:

India’s digital credit boom is real, but so are the risks.

Fintechs that fail to manage complexity will not survive 2025’s regulatory and market reality.

The New Battlefield: FraudTech

If lending was the first phase of India’s fintech revolution,

FraudTech is the second.

As fraud becomes more sophisticated, the battlefield has shifted from product innovation to real-time risk defense. The fintechs that win will be the ones that can detect, predict, and prevent fraud at scale.

Why Fraud Detection is Now the Core Fintech Capability

Fintech success used to depend on:

· CX

· growth

· speed

· onboarding funnels

Not anymore.

Today’s lenders operate in a threat environment where:

· Fraudsters use AI tools

· UPI transactions happen in milliseconds

· Deepfake KYC can bypass human verifiers

· Device IDs can be spoofed

· SIM swaps can occur silently

Fintechs cannot scale unless they build fraud detection into the product DNA.

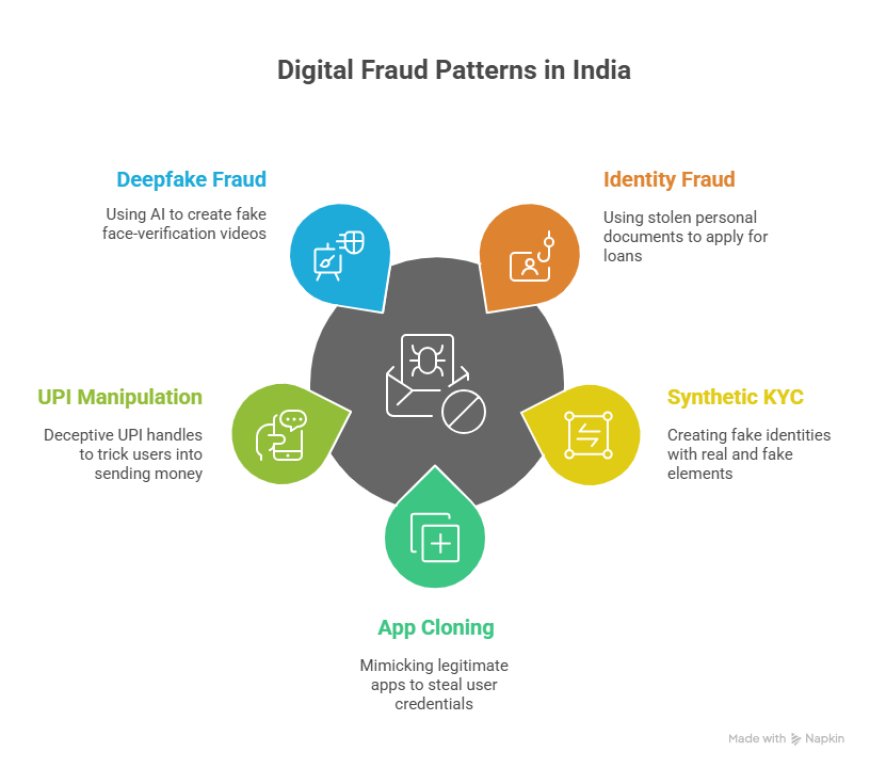

Common Digital Fraud Patterns Rising in India

1. Identity Fraud

Fraudsters use stolen Aadhaar, PAN, or mobile numbers to apply for loans.

This can occur through:

· Data leaks

· OTP interception

· Social engineering

Once the loan is disbursed, the identity owner becomes the victim.

2. Synthetic KYC

A hybrid identity created using:

· Real PAN

· Fake Aadhaar image

· Digitally altered photos

· AI-generated documents

Synthetic KYC is harder to detect because it doesn’t map cleanly to a real person.

3. App Cloning

Fake apps mimic legitimate lending apps or UPI apps.

These clones harvest credentials and drain user accounts.

4. UPI Handle Manipulation

Fraudsters create deceptive UPI handles resembling known brands, banks, or merchants to trick users into sending money.

5. Deepfake-Based Onboarding Fraud

Advances in AI make it possible to:

· Fake face-verification videos

· Bypass liveness checks

· Create realistic human-like synthetic borrowers

This is already emerging as one of India’s biggest upcoming fraud threats for 2025.

Why Legacy Rule-Based Systems Are Failing

Traditional fraud engines rely on:

· Static rules (e.g., block all devices from X geography)

· Basic velocity checks

· Manual approval layers

Fraudsters evolve faster than static rules.

These systems cannot catch:

· Randomized attack patterns

· Synthetic identities

· Behavioral anomalies

· Clustered fraud rings

· Coordinated UPI attacks

Simply put, legacy fraud prevention is obsolete.

The Rise of AI-Driven Behavioral Biometrics & Device Intelligence

FraudTech 2.0 uses invisible, continuous, real-time intelligence:

Behavioral Biometrics

Analyzes how a user interacts with the device:

· Typing rhythm

· Swipe pressure

· Accelerometer data

· Touch patterns

· Gaze & motion insights

These signals are nearly impossible for fraudsters to spoof.

Device Intelligence

Creates a fingerprint of the device through:

· OS version

· sensor data

· global threat feeds

· IP reputation

· emulator/root detection

· device history across apps

This detects mule devices, cloned phones, or fraud farms instantly.

Together, these systems create a risk shield that traditional KYC cannot match.

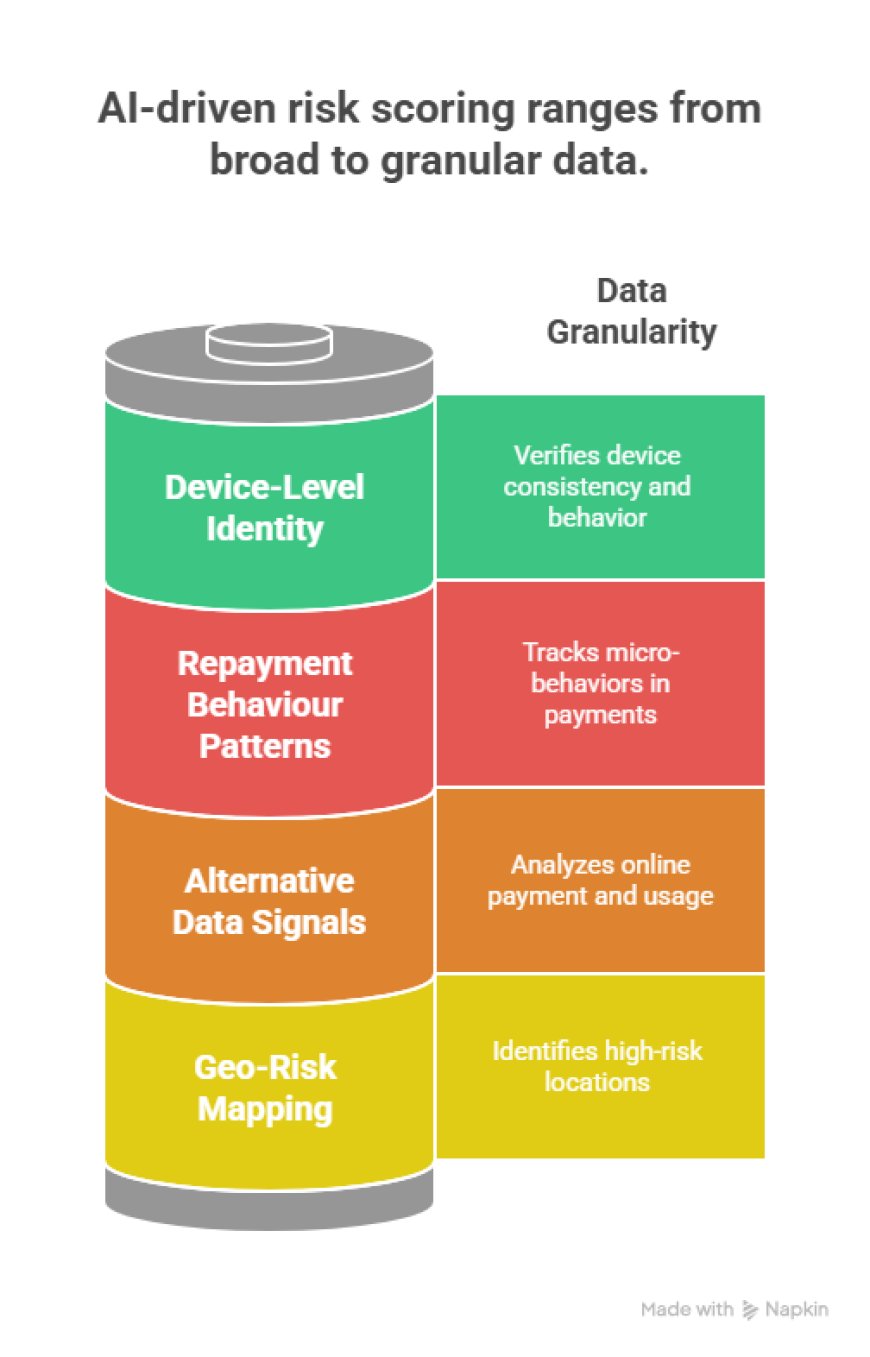

Risk Scoring Reinvented: AI at the Core

India’s fintech ecosystem can no longer rely on legacy credit bureaus or simplistic scorecards. With millions of first-time borrowers entering the formal lending system, risk scoring has become the single most disruptive capability separating compliant lenders from reckless ones.

RBI’s increased scrutiny has pushed fintechs toward Responsible AI—systems that are transparent, explainable, and free from discriminatory biases. This marks a shift from “grow-now, fix-later” to build-risk-first.

The New AI-Driven Scoring Ingredients

Fintech lending models are now reinventing scorecards using multidimensional signals:

1. Alternative Data Signals

Traditional bureau data is often insufficient or nonexistent for new-to-credit users. Modern risk engines now evaluate:

· Payment patterns on UPI

· Utility bill behaviour

· SMS-based income indicators

· Digital footprint patterns (transactions frequency, app usage anomalies)

This helps lenders assess creditworthiness far beyond conventional files.

2. Repayment Behaviour Patterns

AI models now track micro-behaviours such as:

· Timing of EMI payments

· Irregular UPI transfers

· Sudden drop in account balance velocity

· Partial repayments or rollover traps

These time-series patterns enable early detection of distress or fraud.

3. Device-Level Identity

The device is becoming the new Aadhaar.

AI models evaluate:

· SIM-card consistency

· Device fingerprinting

· Jailbreak/root detection

· Behavioural patterns like typing speed or swipe pressure

This layer filters out impersonators and mule accounts.

4. Geo-Risk Mapping

Fraud is often hyper-local. Scoring engines now track:

· High-risk PIN codes

· Unusual geolocation jumps

· Clusters of fraudulent merchant accounts

· Location mismatch between device, IP, and KYC

This prevents fraud rings from exploiting regional gaps.

Real-Time Scoring Becomes a Strategic Edge

Earlier, risk scoring happened at onboarding. Now, it happens continuously:

· During login

· During transactions

· During repayment cycles

· Even during app navigation

Apps that refresh risk scores every few seconds can stop fraud before money leaves the system.

Bottom line:

Fintechs that deploy real-time, AI-powered risk scoring not only reduce NPAs, but also win trust with regulators and users. This is the new competitive moat.

UPI: India’s Digital Backbone Under Attack

UPI has become the world’s most successful real-time payment system — but scale invites attackers. Daily transactions cross 1,200 million, creating an irresistible target for scammers, mule networks, and AI-enabled fraudsters.

Why UPI Fraud Is Exploding

Three major shifts have accelerated UPI-related fraud:

1. Faster payments = Faster fraud

UPI’s instant transaction model leaves little time for banks to intervene.

2. Social engineering at scale

Scammers use phishing, OTP traps, QR manipulations, and fake customer care accounts.

3. AI-powered impersonation

Deepfake voices, cloned apps, and spoofed identities make fraud more sophisticated than ever.

The result: Rising complaints, longer disputes, and pressure on payment providers to tighten security.

New RBI Policies to Strengthen the Rails

To combat fraud, RBI has introduced multiple guardrails that reshape the ecosystem.

1. Request-to-Pay Alerts: More Visibility for Users

UPI apps must now show:

· Clear warnings for collect requests

· Verified merchant badges

· Risk alerts for unknown handles

This helps reduce accidental approvals.

2. App-Level Fraud Locks

Applications are being compelled to add built-in controls such as:

· Daily transfer limits

· High-risk merchant blocks

· SIM-swap detection

· Inactivity-based locks

Users are guided to safety without friction.

3. Real-Time Anomaly Detection

Banks and apps must now deploy intelligence that monitors:

· Suspicious payment patterns

· High-velocity transfers

· Inconsistent device IDs

· Rogue network behaviour

· Multiple failed PIN attempts

These signals trigger instant freezes.

The Future: Hyper-Secure UPI Rails

UPI 3.0 and beyond will transform India’s payment security landscape:

Secure QR Codes

· Encrypted merchant QRs

· Verified merchant overlays

· Anti-phishing watermarking

Biometric Authentication

· UPI with face/voice biometrics

· Aadhaar-powered device binding

· Fingerprint-based approval for high-value payments

Micropayment Risk Scoring

Every ₹1 transaction will soon be assigned a real-time fraud score.

High-risk transactions may require extra authentication.

The Big Picture

UPI’s next era is about frictionless security.

Fintechs that innovate in fraud detection, identity verification, and secure payment flows will define the future of India’s digital economy.

Compliance as a Competitive Advantage

For years, compliance was treated as a mandatory checkbox — something fintechs handled only when raising capital or facing regulatory reviews. But the 2025 reset has flipped this mindset entirely. Compliance is now a product, a differentiator, and the single biggest trust-building mechanism in the Indian financial ecosystem.

Fintechs that treat compliance as a core product win

In a market where customer trust can collapse overnight and RBI actions can alter business models instantly, compliance-first companies enjoy:

· Lower regulatory friction

· Better investor confidence

· Reduced fraud losses

Higher customer retention

· Stronger partnerships with banks/NBFCs

The smartest fintechs are evolving from “growth at all costs” to “trust at all costs.”

Their biggest moat? A system that cannot be gamed, exploited, or misused.

How modern fintech stacks embed compliance

Today’s winning fintech architecture has compliance woven into each layer — not added later as a patchwork.

1. Continuous KYC (cKYC 2.0)

· Re-verification at periodic intervals

· Behaviour-based KYC triggers for suspicious activity

· Deepfake-resistant face matching

· Cross-platform identity consistency checks

2. Automated Reporting to RBI & Partners

· API-driven compliance reports

· Automated loan-level audits

· Instant FLDG exposure tracking

· LSP (Lending Service Provider) disclosures

3. AML Checks Built Into the Core Flow

· Transaction pattern screening

· Sanction list checks

· Money mule detection algorithms

· Beneficiary profiling

4. Consent + Data Governance as Mandatory Layers

· Transparent consent architecture

· User data tagging + lineage tracking

· Encryption + tokenization by default

· Limited retention periods to avoid misuse

These controls don’t slow fintechs down — they accelerate scale.

With clean data, transparent processes, and strong governance, fintechs can confidently partner with banks, expand credit lines, and launch new products faster.

Case Studies (Generic) — Who Wins When Compliance Comes First

· A leading BNPL fintech rebuilt its underwriting stack to make KYC + risk checks mandatory at every purchase. Result: a 40% drop in defaults and a stronger partnership with its anchor NBFC.

· A digital-only micro-lender deployed AI-driven fraud detection and device intelligence. Result: 65% reduction in synthetic identities and a 3x increase in sanctioned credit from banking partners.

· A UPI infrastructure startup focussed on secure APIs and compliance-first architecture. Result: they became the preferred partner for major banks looking to upgrade fraud monitoring.

Across the board, the message is clear:

Compliance is no longer a cost — it is the moat.

The New Fintech Archetypes That Will Win 2025

As India enters a compliance-led fintech era, the industry is reshaping itself. Only a few archetypes will dominate the next decade — and they are defined not by speed, but by trust, resilience, and regulatory alignment.

1. Compliant-First Lenders With Transparent Pricing

These companies operate with:

· Fully regulated digital lending flows

· No hidden charges, dark patterns, or predatory fees

· Balance-sheet responsibility rather than excessive FLDG

· Ethical underwriting + real-risk evaluation

· End-to-end audit trails

RBI’s tightening actually favours them — they already operate cleanly.

2. FraudTech-Native Fintechs That Build Trust

These are tech companies first, financial players second.

They excel in:

· Behavioral biometrics

· Device intelligence

· Deepfake detection

· Risk scoring models

· Transaction anomaly detection

As fraud becomes the #1 threat to India’s digital economy, FraudTech-oriented fintechs will be the backbone of secure lending and payments.

3. UPI Infrastructure Players Powering Secure Payments

India’s UPI stack is evolving from “fastest payments” to “safest payments.”

The winners here will be:

· UPI FraudTech engines

· Secure QR providers

· Biometric authentication layers

· RTP (Request-to-Pay) validators

· Real-time transaction firewalls

These players will become indispensable partners to banks and payment apps.

4. Partnership-Driven NBFC + Fintech Models

The next wave of winners will not try to do everything themselves.

Instead, they will build deep partnerships across:

· Banks (capital & compliance)

· NBFCs (balance sheet strength)

· Fintechs (UX, underwriting, onboarding)

· FraudTech startups (risk & security layers)

This tri-model ensures scale without compromising trust.

Why Capital Will Flow Only to Compliance-Strong Models

VCs, banks, and global investors are now evaluating fintechs on:

· Governance quality

· Fraud loss ratios

· KYC/AML hygiene

· Data protection maturity

· Audit readiness

· Alignment with RBI guidelines

High-burn, grey-area fintechs will struggle to raise capital.

Compliance-strong models, on the other hand, will attract premium valuations because they de-risk the entire financial ecosystem.

What Happens to the Rest?

The fintech landscape of 2025 is no longer a playground — it’s a pressure test. And while compliant, fraud-resilient players rise, the rest face a harsh reality.

High-risk lenders get squeezed out

Fintechs that relied on aggressive acquisition, high-risk borrower segments, and loose underwriting suddenly find themselves exposed.

RBI’s stricter rules around balance sheet responsibility, collections, and KYC discipline mean:

- reckless BNPL models become unviable

- lenders with poor repayment hygiene see rising provisioning costs

- thin-file borrowers become harder to approve without real risk intelligence

The era of “growth at any cost” is over.

FLDG-heavy models collapse

For years, many fintechs survived by riding heavy First Loss Default Guarantee (FLDG) support from partner NBFCs.

But with RBI’s caps and greater scrutiny:

- FLDG-based pseudo-lenders lose their operational cushion

- fintechs with weak credit models struggle to survive

- only those who can originate quality loans stay relevant

The market is shifting from distribution-led lending to risk-led lending.

Fraud-prone apps lose UPI access

RBI’s stance on UPI fraud liability is clear:

If your platform doesn’t control fraud, your access will be restricted.

Fintechs with:

- repeated mule account flows

- high dispute ratios

- deepfake-driven onboarding issues

…risk being downgraded or removed from key payment and lending rails. Losing UPI access in India’s digital economy is essentially a death sentence.

Market consolidation begins — big players with clean books win

As weaker players exit, the market naturally consolidates.

NBFC-backed super-apps, banks with modern digital stacks, and fraud-focused fintechs start to attract:

- more borrowers

- more merchants

- more institutional liquidity

The next two years will see India’s fintech sector go through a clean-up cycle, leaving behind fewer but stronger, more trusted players.

Conclusion

India’s fintech ecosystem is entering its maturity phase — and with it comes a defining shift from experimentation to discipline.

The new survival formula

To thrive in 2025 and beyond, every fintech must master three pillars:

1. Compliance as a product — not a checkbox

2. AI-powered risk scoring — real-time, contextual, multi-signal

3. Fraud intelligence — device-level, behavioral, and predictive

These three capabilities will determine who earns RBI’s trust, consumer trust, and investor trust.

Trust is the new currency

For a decade, India’s fintech wave rode on innovation, speed, and scale.

Now, the winners will be those who can combine scale with safety.

- Lenders who lend responsibly

- UPI players who secure every transaction

- Fintechs who see fraud protection as a revenue enabler

- Platforms that treat data privacy as a core value

In 2025, trust is no longer a feature — it is the product.

The Fintech Reset is here.

Fintechs now face a clear choice:

Survive through discipline.

Or scale through trust.

Those who get this right will define India’s next decade of digital finance.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0