India’s Climate Fintech Boom Financing the Green Transition

India’s climate fintech boom is accelerating with carbon markets, green lending, ESG scoring, and sustainability underwriting. Learn why India is becoming a global climate finance leader.

India is entering a historic phase in its climate and sustainability journey. With ambitious net-zero commitments, rising environmental scrutiny, and pressure from global supply chains, climate action has shifted from a CSR initiative to a strategic economic priority.

At the same time, the world is seeking new, credible, scalable sources of carbon credits, green financing, and sustainability-linked investments—opening the door for India to position itself as a global climate finance powerhouse.

This is where climate fintech steps in.

Platforms that blend finance + climate data + AI + digital infrastructure are helping organisations measure emissions, access carbon markets, deploy green loans, monitor ESG risks, and unlock climate-linked credit. From MSMEs to large enterprises, the demand for tech-enabled decarbonisation and transparent climate reporting is skyrocketing.

Thesis:

India is rapidly becoming one of the world’s most important markets for climate finance products, powered by digital public infrastructure, forward-looking regulation, and a growing need for credible ESG compliance.

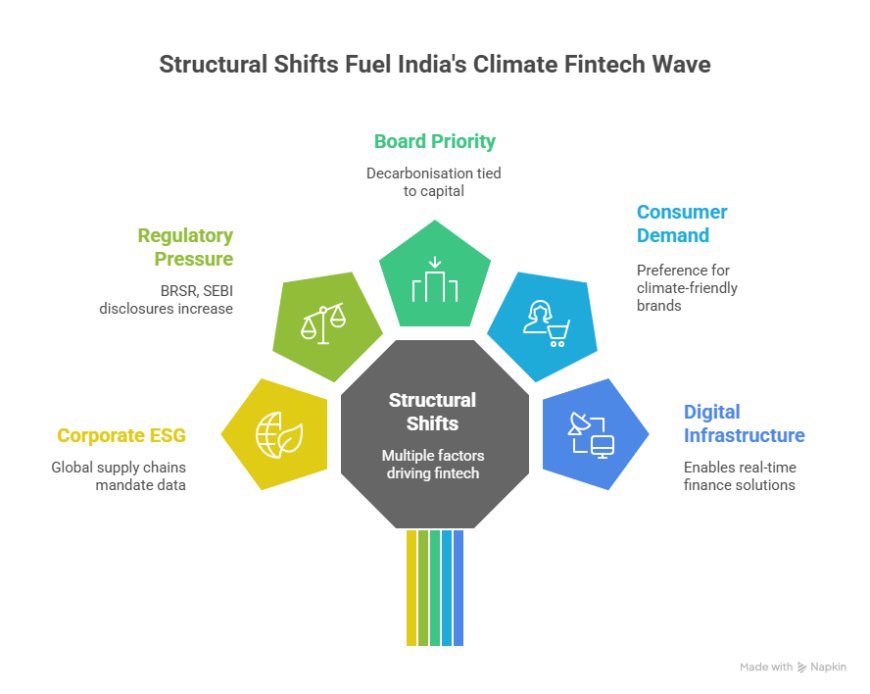

What’s Driving India’s Climate Fintech Wave

India’s climate fintech explosion is not accidental — it’s being fuelled by multiple structural shifts:

a) Corporate ESG Mandates from Global Supply Chains

International brands now require detailed emissions data (Scope 1, 2, 3) from Indian exporters. This is forcing Indian manufacturers, suppliers, logistics players, and MSMEs to adopt digital sustainability tools to stay globally competitive.

b) Regulatory Pressure: BRSR, SEBI Disclosures & Carbon Neutrality

SEBI’s Business Responsibility and Sustainability Reporting (BRSR) norms are pushing listed companies toward high-quality ESG reporting.

Meanwhile, climate disclosure frameworks are becoming mandatory across industries, raising the demand for auditable, data-backed platforms.

c) Decarbonisation Becomes a Board-Level Priority

Energy transition, renewable adoption, and carbon reduction are now tied directly to:

- Capital access

- Brand trust

- Global market acceptance

- Cost optimisation

CFOs and sustainability heads are turning to climate fintech tools to monitor, reduce, and finance their emissions.

d) Rise of Sustainability-Conscious Consumers & Investors

Consumers prefer climate-friendly brands. Investors reward sustainable businesses with better valuations.

This is accelerating adoption of green loans, impact-linked financing, and retail climate products.

e) India’s Digital Infrastructure Enables Scale

Platforms leveraging UPI-like scalability — APIs, satellite data, IoT, blockchain, and DPI rails — are enabling real-time, transparent climate finance solutions across sectors and geographies.

Carbon Credits Go Digital: The New Green Asset Class

Carbon credits are becoming one of India’s most valuable new digital asset classes.

a) India’s Massive Carbon Credit Potential

Sectors like agriculture, renewable energy, waste management, forestry, and MSMEs have millions of untapped tonnes of carbon reduction value.

Climate fintech startups are enabling these sectors to participate in carbon markets by simplifying verification and monetisation.

b) Digitisation of Measurement & Verification

Traditional carbon measurement is slow and expensive. Now, digital MRV (Measurement, Reporting & Verification) tools are transforming the process using:

- Satellite imagery for forest and land-use changes

- IoT sensors for real-time energy and emissions data

- AI models to calculate carbon sequestration

- Mobile apps for on-ground project validation

These tools reduce cost, increase accuracy, and make smaller projects viable.

c) Carbon Marketplaces Gain Momentum

Digital marketplaces are making it possible for:

- Businesses to buy verifiable carbon credits

- Farmers, MSMEs, and renewable projects to sell credits

- Enterprises to track and retire credits transparently

This democratises access and deepens India’s participation in global carbon trade.

d) Blockchain for Verification & Traceability

Blockchain creates tamper-proof records of:

- How carbon credits were generated

- Who verified them

- Who purchased them

- Whether they were retired

This increases trust and prevents fraud — a major challenge in traditional markets.

e) Ongoing Challenges

Despite the progress, the carbon credit ecosystem faces:

- Integrity issues (verifiability, permanence)

- Double counting risks

- Market fragmentation

- Inconsistent quality standards

Solving these will decide which platforms become trusted leaders in India’s green economy.

Green Financing Platforms: Unlocking Capital for Climate Projects

India’s climate transition requires trillions of rupees in green capital — and traditional lending models cannot meet this demand. This is where digital-first green financing platforms are stepping in, bridging the gap between climate ambition and accessible funding.

a) New-Age Lending for Solar, EV Fleets & Green Buildings

Platforms are emerging that specialise in financing:

- Rooftop solar for homes, SMEs, and housing societies

- EV two-wheelers, three-wheelers, and commercial fleets

- Green commercial real estate and energy-efficient appliances

- Clean mobility infrastructure (charging stations)

These fintechs combine digital onboarding, remote verification, and alternative data to underwrite climate assets more accurately than traditional banks.

b) Embedded Climate Lending with NBFC–Fintech Partnerships

NBFCs are now co-building climate-lending products with fintech startups:

- BNPL for green appliances

- Lease-to-own EV financing

- Green capex loans for small factories

- Energy-efficiency loans for MSMEs

The result: faster approvals, lower interest rates, and tailor-made loan products for green transitions.

c) MSME Decarbonisation Becomes a Massive Credit Opportunity

MSMEs contribute ~30% of India’s GDP — but they also have large carbon footprints, outdated machinery, and rising compliance pressure.

Climate fintechs are enabling:

- Low-cost energy audits

- Financing for cleaner equipment

- Tracking & reduction of Scope 1–3 emissions

- Integration into global green supply chains

This segment alone could unlock a multi-billion-dollar credit market.

d) Green Bonds & Sustainability-Linked Loans Enter the Mainstream

India is seeing rapid adoption of green debt instruments:

- Green bonds funding renewable projects

- Sustainability-linked loans (SLLs) with interest rates linked to emissions targets

- Transition financing for polluting industries moving toward cleaner alternatives

Fintech platforms are digitising issuance, compliance tracking, and investor reporting — making these instruments more scalable.

e) AI Improves Underwriting for Green Capex

AI models are now used to evaluate:

- Energy consumption baselines

- ROI from climate investments

- Equipment efficiency

- Weather & geographical risks

- Supply-chain emissions

This allows lenders to shift from asset-heavy underwriting to data-driven, performance-based lending, unlocking capital for millions of climate-positive projects.

ESG Risk Scoring: The New Compliance Currency

As global supply chains demand transparency, ESG (Environmental, Social, Governance) scoring has become mission-critical for Indian enterprises — especially those seeking global customers or capital.

a) Rising Demand for Automated ESG Scoring

Enterprises, NBFCs, and listed companies now need real-time ESG intelligence to comply with:

- BRSR and BRSR Core

- SEBI ESG disclosure norms

- Net-zero commitments

- Global customer expectations

Fintechs are responding with automated scoring engines that process thousands of data points within minutes.

b) How AI-Powered ESG Scoring Works

Modern ESG scoring systems ingest:

- Supply-chain emissions data (Scopes 1, 2, and 3)

- Energy usage & efficiency metrics

- Waste management & water usage data

- Historical compliance records & violations

- Geographical environmental risks (flood zones, heat stress, pollution)

These signals are converted into dynamic scores that lenders, investors, and auditors can rely on.

c) Why ESG Scores Now Influence Credit & Valuation

Banks and investors increasingly use ESG scores to determine:

- Loan eligibility

- Interest rates

- Insurance pricing

- Investor premiums

- Export compatibility in global supply chains

Companies with poor ESG scores face higher borrowing costs and reduced investor trust.

d) Sector Use-Cases

Manufacturing: emissions hotspots, waste disposal, chemicals

FMCG: packaging impact, sustainable sourcing

Logistics: fleet emissions, route optimisation

Real Estate: green buildings, energy efficiency

ESG scoring is no longer a CSR exercise — it is now a compliance currency.

Sustainability Underwriting: The Next Leap in Climate Finance

Underwriting in finance and insurance is being reinvented through the lens of climate risk — transforming how lenders and insurers evaluate customers.

a) Insurers Now Price Policies Using Climate Models

Climate-driven underwriting incorporates:

- Flood & rainfall patterns

- Urban heat islands

- Air quality & pollution levels

- Soil degradation

- Cyclone risk zones

This data dramatically changes how risks are priced.

b) Real-Time Environmental Data Is Redefining Underwriting

With satellite imagery, IoT devices, and drone monitoring, insurers and lenders can now assess:

- Forest cover

- Crop health

- Water stress

- Roof quality for solar installations

- EV battery health

- Energy consumption patterns

This real-time visibility improves loss prediction and reduces fraud.

c) Impact Across Key Sectors

Agri Insurance:

AI + satellite imagery → accurate crop-loss assessments, faster claim payouts.

Property Insurance:

Risk evaluation based on micro-climate zones, building materials, and flood history.

MSME Climate-Risk Lending:

Underwriting loans using data on emissions, energy patterns, and climate vulnerability.

d) India as the Global Testbed

India’s variety of:

- climates

- crops

- pollution patterns

- population density

- digital infrastructure

…makes it the perfect environment for global sustainability underwriting pilots.

The innovations developed here will likely shape international climate-finance playbooks.

Technology Infrastructure Powering Climate Fintech

India’s climate fintech ecosystem is being built on a powerful stack of emerging technologies that make climate data measurable, verifiable, and financially useful.

Satellite + IoT + AI for Emissions Measurement

Accurate climate action begins with accurate measurement.

Modern climate fintech platforms now use:

· Satellite imagery to track land-use change, crop health, forest cover, and pollution hotspots.

· IoT sensors embedded in factories, farms, and energy systems to measure real-time emissions, fuel usage, and energy efficiency.

· AI-driven MRV models (Measurement, Reporting, Verification) to convert raw environmental data into verified carbon metrics.

This makes carbon accounting more scientific, automated, and credible — essential for global acceptance.

Data Platforms for Climate Reporting & Disclosures

With SEBI and BRSR standards tightening, companies need structured data pipelines.

New climate data platforms offer:

· Automated sustainability reporting

· Scope 1, 2, 3 emissions calculations

· Supplier-level environmental data tracking

· Integrated dashboards for ESG disclosures

These tools are becoming the backbone of enterprise climate compliance.

Blockchain for Carbon Registries

Blockchain is solving one of the biggest issues in carbon markets: trust.

Platforms now use distributed ledgers to maintain:

· Tamper-proof carbon registries

· Traceable carbon credit lifecycles

· Transparent ownership histories

· Immutable verification records

This ensures no double counting and boosts global investor confidence.

APIs for Carbon Footprint Tracking

Climate fintech is becoming plug-and-play.

APIs now help:

· Fintech apps show a user’s carbon footprint per transaction

· E-commerce platforms calculate product-level emissions

· Corporate ERPs automate sustainability metrics

· Banks embed “green scorecards” into lending workflows

This democratizes climate data access across industries.

Climate Data Exchanges & Open-Source Datasets

India is building the early foundations of climate intelligence marketplaces.

These platforms aggregate:

· Weather data

· Emissions datasets

· Renewable energy metrics

· Satellite imagery

· ESG disclosures

Open-source datasets enable startups, researchers, and enterprises to innovate faster and cheaper.

The New Climate Fintech Archetypes Emerging in India

A new generation of climate-focused financial innovators is rising across the value chain.

1. Carbon Credit Marketplaces

Startups enabling:

· carbon credit creation

· tokenization

· quality verification

· trade + retirement

These platforms help farmers, MSMEs, and renewable projects monetize their climate-positive actions.

2. Climate Data Intelligence Platforms

AI-powered engines providing:

· emissions analytics

· sustainability dashboards

· supply-chain risk alerts

· climate scenario modelling

Enterprises rely on them for regulatory compliance and climate strategy.

3. ESG Compliance & Reporting SaaS

These solutions automate:

· BRSR reporting

· ESG scoring

· supplier compliance

· sustainability audits

They are becoming essential for manufacturing, FMCG, logistics, and large enterprises.

4. Green Lending & Embedded Climate Finance Apps

Fintech–NBFC partnerships now issue:

· solar loans

· EV fleet financing

· energy-efficiency loans

· climate-linked MSME credit

AI helps underwrite climate benefits + financial risk together.

5. Insurance-Tech Firms Modelling Climate Risk

Insurtech players use climate models to price risks related to:

· floods

· droughts

· heatwaves

· crop diseases

· urban climate patterns

This improves underwriting accuracy for agri, home, property, and MSME insurance.

6. Consumer-Facing Carbon Tracking Apps

Apps that offer:

· personal carbon footprint scoring

· eco-friendly product recommendations

rewards for sustainable choices

This brings climate awareness directly to India’s growing middle class.

What Could Slow the Boom

Despite strong momentum, India’s climate fintech revolution faces major roadblocks.

1. Lack of Standardisation in Carbon Markets

Different methodologies, registries, and quality standards make carbon credits difficult to compare or trust.

Without global alignment, large-scale adoption remains slow.

2. Data Gaps in Emissions Measurement

India’s fragmented data ecosystem makes it difficult to measure:

· scope 3 emissions

· small-scale industrial pollution

· decentralized agricultural emissions

These gaps limit the credibility of climate finance products.

3. Regulatory Uncertainty

Climate policies are evolving.

Unclear guidelines around:

· carbon trading

· green taxonomy

· disclosure requirements

…create hesitation among enterprises and investors.

4. High Cost of Verification & Infrastructure

MRV systems, satellite data, climate analytics, and compliance tools are expensive — especially for MSMEs and small projects.

5. Risk of Greenwashing

Overstated climate claims can erode trust.

Regulators are beginning to crack down, but weak standards create high greenwashing risk.

6. Slow Climate Adoption Among MSMEs

India’s MSME sector (45% of manufacturing output) often lacks:

· climate awareness

· capital

digital readiness

This slows decarbonisation across the supply chain.

Conclusion

India is no longer just participating in the global climate finance movement — it is helping define its future. With massive digital rails, a fast-evolving regulatory environment, and growing enterprise demand for sustainability solutions, India is uniquely positioned to lead the next wave of climate fintech innovation.

As corporates face rising ESG expectations, MSMEs navigate decarbonisation pressure, and investors look for credible green assets, climate fintech platforms are stepping into a trillion-dollar opportunity. Carbon markets, green lending, climate-risk underwriting, and ESG scoring are shifting from niche solutions to core business infrastructure.

The winners of the next decade will be companies that deeply integrate climate risk, sustainability data, AI-driven intelligence, and financial innovation into their products. India has the scale, the digital maturity, and the regulatory momentum to build world-leading climate finance solutions.

The message is clear:

India’s climate fintech boom is not just an economic opportunity — it is a global blueprint for how technology, sustainability, and finance can converge to drive long-term, planet-positive growth.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0